》View SMM Cobalt and Lithium Product Prices, Data, and Market Analysis

》Subscribe to View Historical Spot Price Trends of SMM Cobalt and Lithium Products

1. Review of Nickel Price Trends in the First Half of 2025

In the first half of 2025, nickel prices exhibited a stepped downward trend under the dual pressures of macroeconomic factors and a surplus in the fundamentals. The operating range of the most-traded SHFE nickel contract gradually shifted downward from 135,000 yuan/mt at the beginning of the year to around 118,000 yuan/mt by the end of June, with an amplitude of 28%, hitting a new low in nearly four years. The price evolution can be divided into four stages:

a: At the beginning of the year, amid macroeconomic factors, nickel ore quotas in Indonesia were approved, but the rainy season constrained ore output. Strong ore prices supported nickel prices oscillating between 130,000-140,000 yuan/mt. In late February, expectations for a delayed US Fed interest rate cut pushed up the US dollar, causing nickel prices to drop to 128,000 yuan/mt.

b: In late March, a new pricing mechanism for nickel ore in Indonesia was announced, leading to a sharp surge in nickel prices to 135,000 yuan/mt.

c: In early April, the escalation of the Sino-US tariff war sparked expectations of a collapse in demand, causing nickel prices to plummet rapidly to 115,000 yuan/mt.

d: In June, nickel prices were in the doldrums and bottomed out: Driven by the domestic "anti-rat race" movement, nickel prices rebounded slightly to 123,000 yuan/mt. By the end of the month, they pulled back again to around 120,000 yuan/mt.

2. Supply and Demand Fundamentals

Supply side, according to SMM data, from January to June 2025, China's domestic refined nickel production reached 196,000 mt, up 28% YoY. The increase was mainly due to the capacity ramp-up of domestic electrodeposited nickel projects. Indonesia's refined nickel production reached 29,000 mt, up 53% YoY. After technological transformation in the first half of the year, the Dingxing project resumed full production, and the Yongheng project continued its capacity ramp-up. In the second half of the year, both China and Indonesia are expected to have new production capacities, and refined nickel production is anticipated to continue increasing.

Demand side, from January to June 2025, the nickel consumption in electroplating was 23,000 mt, with a flat YoY growth rate, accounting for 17% of the total refined nickel demand. The nickel consumption in alloy and special steel sectors was 92,000 mt, with a YoY growth rate of 4.5%, accounting for 67% of the total refined nickel demand. The main increase came from high-temperature alloys. The growth rate of civil alloys was lower than that of military alloys due to the slow economic recovery. Special steel did not see significant growth due to the weak real estate market and the fading effect of early release of future demand in home appliances.

In terms of imports and exports, from January to May 2025, China's cumulative imports of refined nickel were 80,000 mt (an increase of 44,000 mt YoY, or 125%), and cumulative exports were 8.2 mt (an increase of 48,000 mt YoY, or 144%). In the first half of the year, refined nickel imports increased significantly, mainly from Russia, South Africa, and Indonesia. Exports were mainly to LME warehouse locations such as South Korea and Singapore, transferring domestic surplus pressure to the international market.

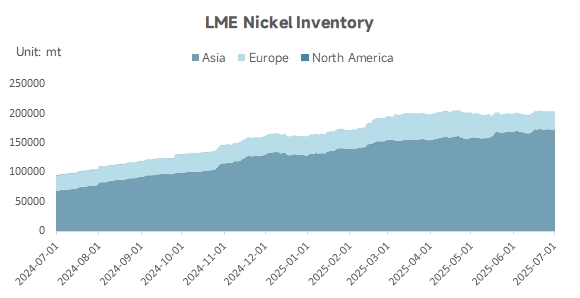

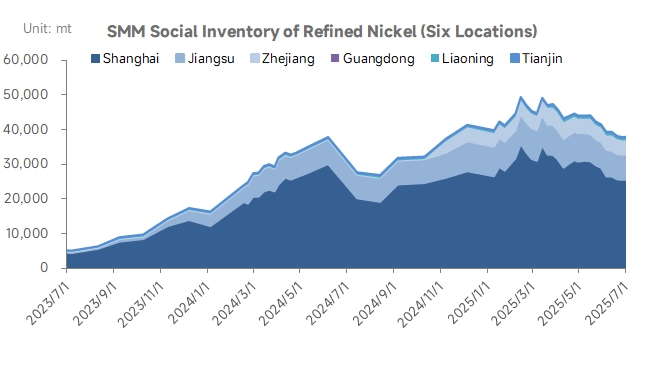

3. Inventory

Nickel inventory shows a differentiated pattern of "increase overseas and decrease domestically": LME nickel inventory has been rising continuously from 160,000 mt at the beginning of the year, currently surpassing the 200,000 mt mark. Surplus nickel resources continue to flow into delivery warehouses, becoming a key factor suppressing nickel prices. However, domestic nickel inventory experienced a slight destocking process in H1. In June, the SMM social inventory of refined nickel in six regions was 38,000 mt, a decrease of 3,000 mt compared to 41,000 mt at the beginning of the year.

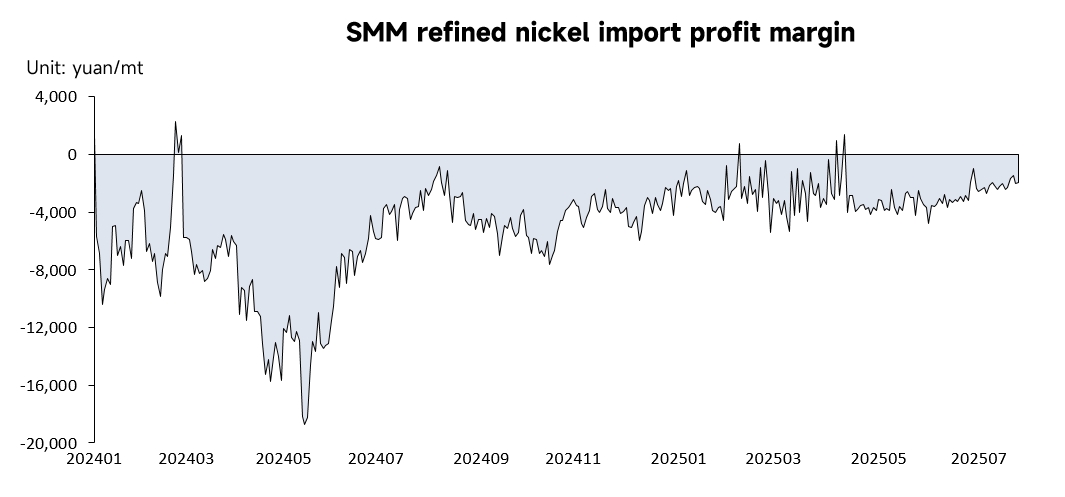

4. Import and Export Profit Margins of Refined Nickel

In recent years, import profit margins have been consistently negative, with only brief periods of import window openings in March 2024 and February and April 2025. With both LME and SHEF nickel prices in a downward trend, due to poor overseas consumption, LME inventory has continued to build up with an increasing magnitude. The inventory pressure is higher than that of SHEF, causing LME nickel prices to fall more sharply than SHEF. As a result, the import loss has been narrowing continuously. As of July 2025, the import loss of refined nickel in China was -1,954 yuan/mt, a YoY decrease of 66%.

Export profit margins have remained positive, except for a short-term significant loss in April 2025 due to abnormal nickel price fluctuations caused by tariff impacts. The overall export profit margins have remained positive in other periods, mainly relying on overseas delivery arbitrage. As of July 2025, the export profit margin of refined nickel in China was approximately $234/mt, a YoY decrease of 64%, with export profit margins also narrowing.

5. Outlook for Nickel Prices in H2 2025

From a macro perspective, there is still significant uncertainty surrounding the US tariff policy. If the tariffs are officially implemented on August 1, it will impact the exports of stainless steel and new energy end-users. Meanwhile, the "Big and Beautiful" Act, which takes effect on September 30, cancels the tax credits for NEVs, further suppressing the demand for ternary batteries. Both factors will weaken the main demand for nickel consumption. In September, if the US Fed cuts interest rates, speculative funds may flood into the nickel market, driving a phased rebound in nickel prices.

In Indonesia, the RKAB approval volume reached 360 million wmt, with only 120 million wmt consumed in H1. To meet targets in H2, mines are expected to increase nickel ore production, and nickel ore prices are anticipated to pull back, further weakening the cost support for nickel prices.

Domestically, China is implementing proactive fiscal and loose monetary policies. The Central Urban Work Conference in July proposed building "green and low-carbon cities" to promote ESS and new energy infrastructure, potentially boosting demand for alloys and high-end nickel materials. Meanwhile, the domestic supply-side reform has significantly boosted market sentiment. The MIIT-led stable growth plan for ten major industries explicitly requires "adjusting the structure and eliminating outdated capacity," particularly targeting high-energy-consuming industries such as steel and non-ferrous metals. However, "outdated capacity" characterized by traditional, backward technology, high energy consumption, and heavy pollution is not prominent in the refined nickel industry. The policy-guided elimination of outdated capacity is expected to have relatively limited impact on the actual marginal supply reduction in the refined nickel industry.

SMM's Summary of Views: The current global macro environment is complex and volatile, with intensified trade frictions and escalating geopolitical risks, exacerbating market concerns about global economic growth. Domestic "supply-side reform" and loose US dollar liquidity provide phased support for nickel prices in H2. However, short-term sentiment fluctuations have not altered the medium and long-term supply and demand logic. Global refined nickel capacity continues to expand in H2, with no significant production cuts yet observed. Demand-side recovery remains sluggish, the electroplating market is relatively stable, and alloy special steel demand has improved but with limited increments. Factors such as increased Indonesian production, tariff impacts, and weak demand still pose downside risks for nickel prices. Overall, it is expected that the tug-of-war between longs and shorts in nickel prices will intensify in H2, with the core fluctuation range being 115,000-128,000 yuan/mt.